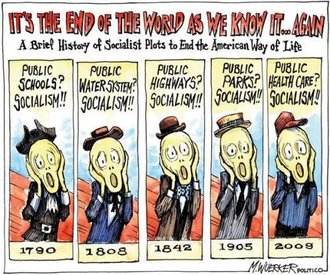

Dear Incoming Members of Congress from the Tea Party,

Do you like clean tap water? How about our scenic and toll-free interstate highways? Do you think 911 service and the fire department are neato?

Then you like taxes! Because taxes pay for all those things, and without taxes, we can’t have them. That’s not socialism–that’s civilization, built up over centuries of debate and experimentation in solving the problems that human societies face.

Have you considered what it would be like to return to a world in which your home would be allowed to burn down if you didn’t display a placard over your door indicating that you’d purchased the right kind of private fire insurance? Do you know why we don’t do that anymore? Because we tried it, and it didn’t work. Some problems cannot be reduced to individual property and individual risk—they can’t be privatized away.

In fact, the richer you are in the United States, the more you make out like a bandit in terms of the benefits you enjoy versus your share of tax burden. Take it from a guy who is much, much richer than you will ever be:

There’s class warfare, all right, but it’s my class, the rich class, that’s making war, and we’re winning.

Now that we’ve got that cleared up, please send in the social conservatives. Salt N Pepa want to have a little chat with them about Don’t Ask Don’t Tell.

Just back from China, where consumption-driven economic strategy is changing the country so quickly that it’s barely recognizable since my last visit just four years ago. Some of this must be due to the Beijing Olympics and the 2010 Expo in Shanghai, but—as the New York Times pointed out a few weeks ago—a lot of it stems from economic policy. After decades of global dominance as a producer of goods, China has become a formidable consumer economy too, producing shock-and-awe-inducing spectacles like this Louis Vuitton flagship store in Shanghai:

Check out the pedestrians dwarfed by the giant LV trunk! This begs for a GIF in which the trunk opens its maw to intone, "Resistance is useless! Open your pocketbooks!"

These and other impressions of China at the end of the first 21st-century decade called to mind an observation made nearly 200 years ago by—of all people—the Scottish novelist, poet and playwright Sir Walter Scott. Not a guy I would have expected to hold views on things like consumer behavior and investing, but apparently he was a man of many parts! Most significantly, worked for many years as a lawyer, giving him at least a passing interest in things like the legal revival of the corporation in England, through the 1825 repeal of the Bubble Act.

Sir Walter Scott: novelist, poet, lawyer, and economic visionary.

As Scott pointed out, even in the early days of the Industrial Revolution, consumption was at least as important as production as an “engine” of economic development. Not only that, but he argued—in a way that would be at home in many contemporary policy discussions—that consumption was the driver of growth in financial markets. That is, increasing the value of investments depends on consumer behavior.

Even in the infancy of the contemporary global economy, apparently, it was clear to Scott and others that the way to make money was by spending it. The industrial economy, he said, was like a hydraulic engine: it produces water as a byproduct of its operation, but then uses that water as fuel. In the same way, he wrote, joint-stock corporations produce consumer goods, the consumption of which fuels corporations economically. Thus, an investor increases corporate profits when he:

…buys his bread from his own Baking Company, his milk and cheese from his own Dairy Company…drinks an additional bottle of wine for the benefit of the General Wine Importation Company, of which he is himself a member. Every act, which would otherwise be one of mere extravagance, is, to such a person…reconciled to prudence. Even if the price of the article consumed be extravagant, and the quality indifferent, the person, who is in a manner his own customer, is only imposed upon for his own benefit. Nay, if the Joint-stock Company of Undertakers shall unite with the medical faculty…under the firm of Death and the Doctor, the shareholder might contrive to secure his heirs a handsome slice of his own death-bed and funeral expenses.

—from the “Introduction” to The Betrothed, 1825, p. 6

Now this shop-and-spend approach is reshaping China, and through China, the whole distribution of global economic power. The striking and surprising thing, to me, about the Scott quote is how early he spotted what would become the dominant economic policy motif of contemporary capitalism. To his long list of roles and achievements, let us add “economic visionary.”

Behavioral finance has exploded in popularity not just because it’s interesting—regular finance is interesting, too—but because it combines that interest factor with an abundance of what one scholar called “descriptive charm.”

There is something strangely entertaining in reading about the economic foibles of others: one part schadenfreude, plus one part abashed recognition of one’s own past mistakes—mixed with quiet relief to find oneself with lots of company in making those mistakes.

Reading behavioral finance can also provides a sense of Finally Understanding How Things Work when it comes to money and markets. Learning about common cognitive errors in economic decision making, such as “anchoring,” and “availability bias,” feels like getting a peek inside the flawed machines that are our brains, making it seem possible to predict the behavior (particularly the mistakes) of others, and guard against them in oneself. In short, behavioral finance seems to offer insight and a sense of control, imposing order on what otherwise appears chaotic and unpredictable.

All research programs have limitations, of course. But those of behavioral finance undermine its purpose: that is, to enhance understanding of financial markets and investor behavior. Others have written eloquently on this subject, particularly Daniel Beunza and David Stark, and John Y. Campbell. What I have to add to this ongoing debate boils down to two points and their consequences:

1. Failure to acknowledge the findings of the allied social sciences

One of the cardinal laws in scholarship is to acknowledge the work of others and avoid reinventing the wheel. But when you read works of behavioral finance, you’d never know that deviations from rational, self-maximizing behavior are old news in psychology, political science, sociology and anthropology. Check the references section of a behavioral finance article or book and see how many citations from those fields you can find. Chances are, there will be zero. Behavioral finance scholars generally cite each other, or work from mainstream economics and finance.

This is particularly strange since so much of contemporary behavioral finance depends on the contributions of social psychologists like Daniel Kahneman (a 2002 Nobel laureate for his work in behavioral finance) and the late Amos Tversky, as well as much older work by people like Herb Simon, who was a Professor of Political Science and Industrial Administration at various points in his career. Simon won the Nobel Prize in economics for work done half a century ago on “bounded rationality“—a concept closely tied to many of the key phenomena examined by behavioral finance, but which is virtually ignored in their publications.

While a lot of academic research speaks to a rather small group of other academics, behavioral finance is distinctive within the social sciences for restricting its scholarly conversation so tightly. This isn’t the case in the closely-related disciplines of economic sociology, neo-institutionalist political science, and economic anthropology, all of which regularly cite and engage with one another, to the enrichment of all.

In the case of behavioral finance, reluctance to acknowledge the many research interests it shares with the allied social sciences may be part of the larger project of rigid separation and boundary enforcement that has been carried out by economists since the time of Pareto. This has created what Schumpeter described as a regime of “mutual vituperation” which has kept economics and finance in a state of self-imposed incommunicado with sociology, limiting the advancement of knowledge on our shared interests. Behavioral finance, it seems, is sticking to the party line on this point.2. A narrow, limited critique of economic theory

Cataloging the many ways humans fail to think rationally about money, investments and risk is a good start. But in most ways, behavioral finance leaves intact the problematic assumptions of traditional finance, pulling its punches, so to speak. Among the most noteworthy examples:a. Behavioral finance remains stuck at the individual level of analysis

As in traditional finance and economics, the object of inquiry in behavioral finance is the individual—despite rafts of evidence going back decades that individuals don’t make decisions about money, risk or investing in a vacuum, but as a result of social influences. Of course, this evidence comes from those allied social sciences that are being so studiously ignored. For example, economic psychologist George Katona showed 35 years ago that most people choose investments based on word of mouth recommendations from their friends and neighbors. This influence of social forces in economic decision-making has been demonstrated with equal or greater impact among finance professionals—for instance, in a study of Wall Street pension fund managers by economic anthropologists O’Barr and Conley, and more recently in a sociological study of arbitrage traders by Beunza and Stark.

In the past, there were encouraging signs that behavioral finance might break through the limitations imposed by sticking to the individual level of analysis, most strikingly in Robert Shiller’s 1993 statement that “Investing in speculative assets is a social activity.” But thus far, the implications of such statements, and the plethora of evidence supporting them, remain unexplored.b. Behavioral finance limits itself to pointing out failures of cognition and calculation As important as those factors are in distorting financial decision-making, there are a host of others that we know about—based on research in those allied social sciences that behavioral finance doesn’t acknowledge—that are excluded from research in behavioral finance. This includes emotions, and social phenomena like status competition, both of which play a significant role in the findings of economic sociology, psychology and anthropology. The cognitive/calculative failures may interact with the socio-emotional phenomena, but we won’t know as long as behavioral finance pretends the latter don’t exist. That’s a loss for all of us interested in markets, money and investing. c. Behavioral finance doesn’t explain how individual acts and decisions produce aggregate outcomes As a consequence of keeping the analytical focus on individuals—avoiding the social and interactive aspects of economic activity—behavioral finance doesn’t have the theoretical means to address mechanisms through which individual acts and decisions aggregate. That means it can’t explain institutions and other manifestations of collective behavior which form the context for all the individual behavior it examines. Of course behavioral finance can’t answer all questions about money and markets, but it ought to be able to explain what happens when hundreds, or hundreds of millions, of people fall prey to the “hot hand” fallacy or availability bias? If behavioral finance won’t touch questions like that, who will?

The consequences for ignoring the other social sciences and mounting a very narrow critique of traditional finance and economics, include:

Limited predictive power

Behavioral finance tells us more about what people won’t do (e.g., behave according to notions of rationality outlined in economic theory) than what they will do.

Contradictory implications

Are investors risk-averse or overconfident? How should we reconcile seemingly contradictory findings like these? Behavioral finance doesn’t tell us, because of its…

Failure to offer a viable alternative to the theories it challenges

Pointing out all the ways that real life behavior doesn’t bear out the predictions of traditional economics and finance is interesting—even fascinating, at times—but it’s not an alternative theory. “People aren’t rational” isn’t a theory: it’s an empirical observation. An alternative theory would need to offer an explanation, including causal processes, underlying mechanisms and testable propositions.

All this keeps behavioral finance dependent on traditional economics and finance rather than allowing it to grow into a robust theoretical realm in its own right. Perhaps someday the field will develop into something more truly challenging to economic orthodoxy. Until then, behavioral finance will have to play Statler and Waldorf to the Muppet Show of mainstream finance—providing entertaining critique, but not replacing the marquee acts. (Now if economics would just substitute Milton Berle for Milton Friedman….)

Can you guess the decade in which the following words were written? How about the century?

…a certain class of dishonesty, dishonesty magnificent in its proportions, and climbing into high places, has become at the same time so rampant and so splendid that men and women will be taught to feel that dishonesty, if it can become splendid, will cease to be abominable.

This quotation is from the 50s. The 1850s, that is. And the author was prolific British novelist (and postal service employee!) Anthony Trollope. The reflections on dishonesty come from his 1856 Autobiography, but he is probably best-known for his novel of greed and fraud, The Way We Live Now.

Anthony Trollope, 1815-1882

Trollope’s most famous creation is undoubtedly the flamboyant con artist Augustus Melmotte,to whom Bernard Madoff was often compared in recent years. In fact, a comparison between the two is illuminating. Like Madoff, who built his hedge fund on a “big lie,” Melmotte conjured a fortune out of smoke and mirrors, through moves like selling shares in a railway that never existed. And both parlay wealth into access to positions of social prominence and public trust—Melmotte buys a seat in Parliament, while Madoff chaired NASDAQ for several years during the 1990s. Life imitating art, or just tragedy following farce?

This kind of financial chicanery, “dishonesty magnificent in its proportions,” was very much on Trollope’s mind in 1856 because English law had recently re-legalized and expanded the rights of the joint stock company—the ancestor of the modern corporation, and a form of business enterprise so tarnished by fraud that it was outlawed for over a century in the UK.

What, you might ask, was the big deal? Why get so exercised about a change in the legal status of an organizational form?

Four words: the South Sea Bubble. Also known as the world’s first great financial fraud, the Bubble was so destructive to England’s economy and society that Parliament banned all new incorporations (with a very few exceptions) for more than a century.

The Bubble arose around the stock of the South Sea Company, an entity created by act of Parliament to trade exclusively with the Spanish colonies in South America—and, not incidentally, to rid the British Crown of a crippling national debt by raising capital through the sale of shares.

Investors flocked to buy the company’s stock, which rose dramatically, by sixfold in one year, and then quickly plummeted as shareholders, realizing that the company was worthless, panicked and sold. In 1720 — the year a major plague hit Europe, public anxiety about which “was heightened,” according to one historian, “by a superstitious fear that it had been sent as a judgment on human materialism” — the South Sea Company collapsed. Fortunes were lost, lives were ruined, one of the company’s directors, John Blunt, was shot by an angry shareholder, mobs crowded Westminster, and the king hastened back to London from his country retreat to deal with the crisis. The directors of the South Sea Company were called before Parliament, where they were fined, and some of them jailed, for “notorious fraud and breach of trust.” Though one parliamentarian demanded they be sewn up in sacks, along with snakes and monies, and then drowned, they were, for the most part, spared harsh punishment. As for the corporation itself, in 1720 Parliament passed the Bubble Act, which made it a criminal offense to create a company “presuming to be a corporate body,” and to issue “transferable stocks without legal authority.”

It was possible to outlaw the corporate form of organizations because at that time, they required a government charter to exist. If a corporation broke the law, it could be punished by revocation of its charter—sort of like the death penalty for juris persons (“legal persons,” which distinguished the status of corporate actors from that of “natural persons,” i.e., human beings).

This tight legal control was driven by deep suspicion of the corporate form which long predated the South Sea Bubble. In contrast to business partnerships, where the managers were also the owners of the firm, the corporation innovated by separating management from ownership, with the latter belonging to shareholders. Even Adam Smith thought this was a bad idea, warning in The Wealth of Nations that

The directors of such companies, however, being the managers rather of other people’s money rather than of their own, it cannot well be expected that they should watch over it with the same anxious vigilance with which the partners in a private copartnery would watch over their own….Negligence and profusion, therefore, must always prevail, more or less, in the management of the affairs of such a company…They have, accordingly, very seldom succeeded without an exclusive privilege, and frequently have not succeeded with one (1776: 439).

In other words, the corporate form had trouble written all over it. Specifically, it presented a built-in problem of moral hazard by given managers authority over “other people’s money.” Among other things, this created tempting conditions for financial fraud.

All these suspicions were borne out and more by the South Sea Bubble. But by the time of Trollope’s reflections, the memory of the disaster was fading, and the Industrial Revolution was generating tremendous wealth. By 1856, Parliament had not only repealed the Bubble Act, but expanded the powers of juris persons, clearing the way for super-charged economic growth—and for a return to the “magnificent” frauds perpetrated by corporations.

Yet, as Bakan writes, the corporate frauds that have come to light since the re-legalization of the corporation have not provoked anything remotely like the “Bubble Act” in response:

Today, in the wake of corporate scandals similar to and every bit as nefarious as the South Sea bubble, it is unthinkable that a government would ban the corporate form…over the last three hundred years, corporations have amassed such great power as to weaken government’s ability to control them. A fledgling institution that could be banned with the stroke of a legislative pen in 1720, the corporation now dominates society and government.

To Bakan’s power-based explanation—that the power of the corporation has simply outgrown that of the state—we might add Trollope’s notion of public tolerance for fraud in high places. That is, the state doesn’t crack down on corporations because it lacks the popular mandate to do so.

Trollope would probably have appreciated John Kenneth Galbraith’s rueful observation that “There can be few fields of human endeavor in which history counts for so little as in the world of finance.”

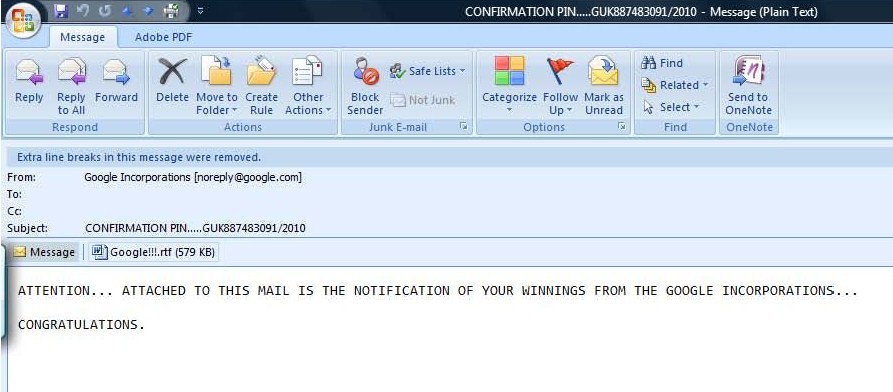

Have you gotten a flurry of these things as well? Emails of an exuberantly preposterous nature, full of rip-snorters that make you wonder how the authors managed to create such a sublime pastiche of accurate and absurd, plausible and im-?

Apparently, there are LOTS of other “winners.” And thanks to the many websites that seek to expose internet scams, it’s possible to read several versions of this email. Reading across versions allows several interesting patterns emerge.

Scam Emails as a Literary Genre

On the one hand, it suggests that scam letters can be read as a kind of literary form in their own right—an insight, I’m happy to say, that has been offered by others, notably Scam-O-Rama, which notes that scammers’ missives “smack of political satire, [and] contain elements harking back to 19th century literature.” If you can get past the jarring confusion about the words “Corporation” and “Incorporation” (plus the random plural added to the latter), the authors of the “Google Incorporations” series have a virtually Dickensian flair, from the names they invent for the letters’ authors to their conceits about why and how Google is distributing its largesse.

Two literary aspects of the letters stood out to me:

The names

Most versions of the letter are putatively authored by someone bearing the title of “Doctor.” Whether this is supposed to connote a medical credential or a doctorate is unclear—that’s part and parcel of the strategic ambiguity employed throughout the letters. The names themselves range from the mundane (“Dr. Frank Smith” or “Dr. Nelson Cole”) to the more memorable (“Dr. Kibbs Richardson”). One particularly flamboyant letter is authored by a certain “Sir Richard Scholes,” purportedly the “Foreign Transfer Manager” for Google. Because of course a British lord would occupy a middle management position at an American high tech company. My personal favorite is “Dr. Paul Zimmaman”—written as if by a person who has never seen “Zimmerman” written out, but has heard the name spoken and just spelled it as it sounded.

The vocabulary

This seems to be one of the defining characteristics of SPAM “literature” in all genres, not just the “Google Incorporations” series. For whatever reason, scammers just love the word “hence.” As in “Hence we do believe with your winning prize, you will continue to be active and patronage to the Google search engine.” So that’s -1 for inability to distinguish between a noun and a verb (“patronage”), but +1 for the “Hence”?Running a close second is the word “therefore,” as in “You have therefore won the entire sum of ?450,000.00 {Four Hundred And Fifty Thousand Great British Pounds Sterling} and also a certificate of prize claims will be sent along side your winning cheque.” A certificate! Making things even more official!

Making things seem official is the name of the game: for instance, you aren’t just asked how you want to get your money, you have to “select your mode of prize remittance.” Prolixity FTW!

Global Capitalism as Seen from the Periphery

Secondly, the “Google Incorporations” letters can be read from a more sociologically analytical standpoint, for what they tell us about the mental models some people hold of the contemporary global economy. In this sense, the letters can be savored both as unintentional comedy and as commentary on how capitalism is understood in some parts of the world.

The assumptions underlying the “Google Incorporations” series are revealing as accounts that the authors think will be plausible to readers (e.g., potential victims or “marks”). Obviously, the authors know that Google isn’t giving away money, but they’re hoping to create a convincing illusion.

My interest lies here: the pastiche of capitalism that the scammers are producing. What features do they consider indispensible to creating that illusion? The many ways in which they fail to portray corporate activity realistically are glaringly obvious. But I’m interested in what they think is going to fly with readers—at least well enough to get readers to cough up the personal data the scammers are seeking.

Spatial indeterminacy

Google’s geographical location turns out to be one of the things that the scam letters’ authors don’t consider very important to making their appeals convincing. Mimicking a standard business letter, the Google Incorporations “award notification” leads with the firm’s address. But the address is in the UK!

Google Incorporations.

Stamford New Road,

Altrincham Cheshire,

WA14 1EP

London,

United Kingdom.

Leaving aside the plausibility problem of situating one of the world’s leading tech firms in the UK rather than the Silicon Valley, the authors apparently don’t have a very good grip on English geography.While there is actually a Stamford New Road in the town of Altrincham, Cheshire, that town is several hundred miles northwest of London.

It looks to me as if the authors just randomly added “London” between the postcode and the country name, much as they added the random “s” at the end of the word “Incorporation.” Because dropping the name of the international capital of finance can only help, amirite?

The prize giveaway: corporations as cargo cults

Here’s where things really get interesting, in my view.In the world of the “Google Incorporations” authors, corporations are mysterious entities that dispense large chunks of money on a whim. A sum approaching three-quarters of a million US dollars just to “thank” loyal customers? No problemo!

Adding to the mirth, the give-aways are purported to occur via lottery—a lottery that “winners” never entered in the first place. It makes the corporate world seem like a kind of modern cargo cult, dumping wealth haphazardly upon the unsuspecting.

A cargo cult, as Wikipedia informs us,

“is a religious practice that has appeared in many traditional tribal societies in the wake of interaction with technologically advanced cultures. The cults focus on obtaining the material wealth (the “cargo”) of the advanced culture through magic and religious rituals and practices. Cult members believe that the wealth was intended for them by their deities and ancestors.”

The cargo cult originated in Melanesia, where planes would drop cartons of food and so forth from the sky, much to the surprise of the local population. New beliefs sprung up around this experience, along with new rituals designed to get the mysterious flying objects to come back and dispense more wealth.

In a way, this is a very sensible interpretation of capitalism: people get rich, seemingly at random. It’s as if money just drops out of the sky onto their heads.

The premise of the “Google Incorporations” letter—and, I would argue, lotteries in general—can be summed up by the idea “it could happen to you, too!”

This wistful thought may explain why so many people ignore the obvious signs that these “award notifications” are frauds, and post to scam-exposé websites, asking plaintively whether the offers could possibly be legit. It’s all very reminiscent of Pearl Bailey’s appeal to Santa for a “Five Pound Box of Money:”

Economists have an interesting relationship to the empirical world. You’ve probably heard the one about the economist walking down the street with a friend and noticing a $100 bill lying on the ground. As the friend bends over the pick up the bill, the economist says, “Don’t bother—if it were a real $100 bill, someone would have picked it up already.”

So when an economist starts talking about empirical support for a theory, it’s sort of a special occasion. Thus the Quote of the Month selection for September:

“…there is no other proposition in economics which has more solid empirical evidence supporting it than the Efficient Market Hypothesis.”

It probably goes without saying, as we approach the two-year anniversary of the Great Crash of 2008, that Jensen’s comment hasn’t worn well over time. In fact, anyone who has been paying attention to the last 30 years in the stock market is going to have a tough time accepting the Efficient Markets Hypothesis, which asserts that market prices fully reflect all available information.

Where was the EMH when the skeletons of the subprime mortgage crisis started to fall out of the closet? Let’s mosey on back to July 2007 to see.

At the same time, the Dow Jones Industrial Average was hitting a new record high of 14,000. Remember Dow 14,000? So what information was the market reflecting, exactly? Maybe this:

Adam Smith, economist and moral philosopher, 1723-1790.

Adam Smith observed in his Lectures on Jurisprudence (1762)–a series of talks that he gave at the University of Glasgow– that national character plays a significant role in economic transactions: the Dutch, he said, are “more faithful to their word” and better at “performing agreements” than the English, and the English more faithful than the Scots.

In the past few months, I’ve observed a similar kind of cultural variation in a much more prosaic setting: the panhandling interaction.

If you’re from North America, as I am, you’ve probably seen people on the street requesting money from strangers using appeals such as “Homeless—Please Help” or “Homeless Veteran.” There are a number of variations, but homelessness is the common theme in many cases.

A sampler of panhandling signs from the US.

Elsewhere in the world, panhandlers use quite different rationales—or what the great mid-century sociologist C. Wright Mills would call “vocabularies of motive.” Mills wasn’t interested in what actually motivated people—such as what psychologists would term “needs” or “drives”—but rather in the ideologically-charged terms they used to justify their actions to themselves and others. As he observed, some motives are more acceptable than others, and we can learn something about local cultures based on what passes for a “good reason.”

C. Wright Mills---the most dashing of sociologists.

So it’s sociologically interesting that within the North American context, the concept of “home” has such resonance that the claim of “homelessness” is considered a compelling and sufficient motive for giving money to strangers. But while the need for shelter would seem universal, it’s rare to see a panhandler outside North America requesting a donation on the basis of homelessness.

In Germany, for example, one often finds people begging for “trinkgeld”—“drinking money.” And they’re not playing for laughs, as one sometimes finds in the US, when panhandlers give a wink and a nod to the stereotype that money given to beggars is only ever used to buy alcohol (or drugs). When a panhandler asks for “drinking money” in the US, it’s sort of an in-joke, or an attempt to appear disarmingly honest; based on the limited examples I’ve seen, this seems to jolly people up and get good results (i.e., quantities of cash).

But in Germany, drinking money is serious business. In the four years I lived in the Rhine Valley, I saw dozens of men (always men) on public transport and on the street, asking for “trinkgeld, bitte” in monotonous, dirge-like tones that seemed to express just how grim a fate it was to lack beer money. Equally surprising to me was the willingness of Germans to open their purses for this reason, as if it was a truth universally acknowledged that a man with empty pockets must be in want of a beer. In the interactions I witnessed, no one on either end of the transaction ever smiled.

Panhandling in Istanbul.

Yet another vocabulary of motive can be found on the streets of Istanbul, where panhandlers often approach passers-by with a request for “ekmek parası”—Turkish for “bread money.” In perhaps 10 visits to Turkey in the last 3 years, I’ve never seen anyone on the street claiming to be homeless. Nor have I seen a cardboard sign of the kind so common in North America.

In all three settings, the vocabularies of motive among panhandlers have a common theme of need: for shelter, drink or food. What’s interesting is how each cultural setting changes the calculus about what kind of motive is most likely to bring in the cash. Perhaps it comes down to what each society views as among the basic human rights: in the US, shelter has a plausible claim to that status, but beer does not; whereas in Germany, it an appeal for “trinkgeld” succeeds as an appeal to common humanity and decency; in Turkey, hunger seems to trump all other claims.

Have you seen other variants in national culture and vocabularies of motive when it comes to panhandling? Your examples (and analyses) are welcome.

After a brief hiatus, Quote of the Month Club is back from summer vacation with this gem from POTUS #33, Harry S. Truman:

It’s a recession when your neighbor loses his job; it’s a depression when you lose yours.

—quoted in the Observer magazine, 13 April 1958

Old Harry knew a thing or two about recessions, having lived through over a dozen by the time he made that comment in the Observer.

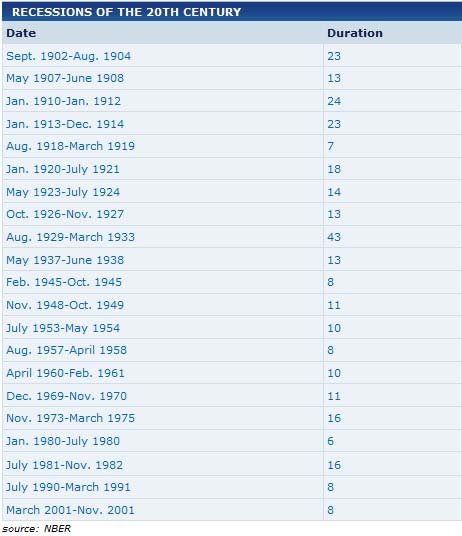

In fact, if you are inclined to take consolation in history, you may enjoy this chart from the National Bureau of Economic Research, listing all the recessions that occurred in 20th century America. Should you be feeling glum about our current crisis—now in its 23rd month—check out what was happening a century ago: in 1910, the US was entering its second 23-month recession in a decade! Between 1902 and 1912, the American economy spent a total of five years in the dumps. Ouch.

This has been a public service announcement from the “it could be worse” school of crisis management.Our motto: “When others think they’ve hit rock bottom, we start digging.”

Proof that the world will end not with a bang but a whimper: Snooki saying "Waaah."

.

The S&P Styling Product Index surged higher on Tuesday as the cast of MTV’s “reality” show, The Jersey Shore—including noted economist J-Doww—rung the opening bell at the New York Stock Exchange.

[crickets]

No, seriously! This quasi-apocalyptic event actually holds some interest for economic sociology.

In what may be the ne plus ultra of performative economic action, a group of young people who make their living performing* obnoxious ethnic, class and gender stereotypes appeared on one of the world’s great stages for performing the capitalist market economy.

The event seemed to be greeted with universal dismay, from observers who found the Jersey Shore cast to be insufficiently “true” to their on-screen selves (?!?), to those who saw their presence at the Exchange as a kind of sacrilege, judging by reaction on the NYSE’s Facebook page.

I’d like to suggest that what seems so wrong with that picture of Snooki and company ringing the opening bell actually makes a lot of sense sociologically. If this meeting of worlds—entertainment and the stock market—seems strange, it may be because we’re so used to regarding the markets as “real,” rather than as a performance (or even as entertainment in their own right).

But sociological researchers are building the case for treating markets as no more “real” than “reality TV.” As Michel Callon has written, “economics . . . performs, shapes and formats the economy, rather than observing how it functions” (1998: 2). This theme of economists creating markets was picked up and elaborated by Donald MacKenzie and Fabian Muniesa, who argued persuasively that by describing and predicting market behavior, economists create self-fulfilling prophecies (Merton 1949), thus performing the markets they claim to observe as outsiders. As an example, the idea here is that when economists—or the chief economist of the United States—says the American economy is in recession, it becomes so. The statement makes the situation real rather than conjectural.

Which brings us back to The Situation and friends. Perhaps the most troubling aspect of their appearance at the NYSE is not their incongruity, but how very much they belong there. As performers famous for simulating reality, they have something important in common with economists who perform markets by stimulating the reality they purport to describe.

Both are engaged in producing what French sociologist and cultural theorist Jean Baudrillard calls “the simulacrum:” a copy without an original, a pretense that replaces and ultimately negates “reality” so successfully that we no longer care about what is real.

One sort of simulacrum is the “referent:” someone or something that represents something else, as the cast of The Jersey Shore is purported to represent a segment of American society. Another sort of simulacrum—the dominant type in a post-industrial age—is the model, which becomes more real than the reality it supposedly represents. And model-creation, particularly the development of models that reframe a messy reality in clean and elegant terms, is a specialty of economists.

When Baudrillard said of the simulacrum,

It is no longer a question of imitation, nor duplication, nor even parody. It is a question of substituting the signs of the real for the real… (1994: 2)

…he could have been writing the job description for the Jersey Shore castmates, as well as for the economists whose declarations of recession and recovery animate the markets.

In fact, Baudrillard foresaw the collision of the entertainment and economic spheres through their shared use of models and representations to supplant reality. His body of work, starting with Simulacra and Simulation in the early 1980s and continuing through Impossible Exchange in 1999, implicates Wall Street and academic economics in the same project as Disneyland and Hollywood.

The pageant of the Chicago Mercantile Exchange, produced by artist Andreas Gursky.

Theorized in this light, the market isn’t just performative, but a performance produced for our entertainment—an idea explored visually by artists such as Andreas Gursky and Burak Arikan. Economic reports and analysis thus become part of what Baudrillard’s contemporary, Guy Debord (a founder of the Situationist movement, appropriately enough), termed The Society of the Spectacle:

The language of the spectacle consists of signs of the ruling production, which at the same time are the ultimate goal of this production…The spectacle subjugates living men to itself to the extent that the economy has totally subjugated them.

Theorized through this lens, the image of the Jersey Shore cast ringing the opening bell at the NYSE persists in memory not because it is represents a collision of worlds, but because it brings together two genres of performance whose entertainment value depends on their purported “reality.”

Seeing the two juxtaposed underscores the illusory nature of both types of performance—the “guidos” and “guidettes” appear out of character, exposing their Jersey Shore personas as characters, and suggesting that the NYSE is just another kind of stage. The effect is similar to the “Funny or Die” episode entitled “The Real Jersey Shore,” minus the reassuring label of parody:

___________________

* Their range as performers was showcased in the epic drama “Friggin’ Twilight:”

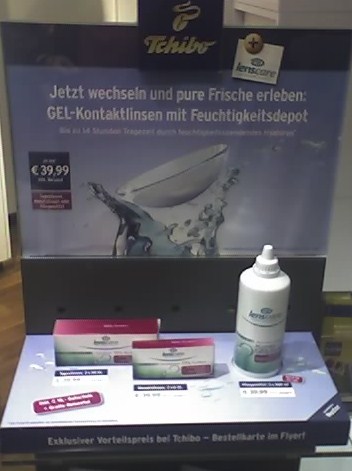

Would you buy contact lenses from a coffee shop? How about a new car? Perhaps some insurance products with your drink?

If you live in North America, these questions probably sound absurd. But it’s the business model of Tchibo—a firm which describes itself in utter seriousness as “Coffee shops also selling housewares, accessories, and clothes.” In practice, this model is even more confusing than it sounds, because—as the official corporate slogan puts it—Tchibo is “A New Experience Every Week.” So, as of June 18th, they’re selling household furniture; a few months ago, it was American country-western clothing (yup, they’ve got both kinds). Next month, who knows?

The Hamburg-based retailer starting selling coffee beans within Germany in 1949, expanding to what the firm coyly calls “non-food items” in 1973 by using their retail space to sell items placed there on consignment by other companies. The “extended product line” started with things that were at least thematically related to coffee and food consumption, like place mats and serving trays. But soon the model spun off into wild new directions, like cars and cowboy boots. And now Tchibo is not only Germany’s largest coffee shop chain, but has expanded into 10 other countries, from the UK to Turkey, with more to come.

Here’s the mystery: this isn’t supposed to work. In fact, what Tchibo does is supposed to be disastrous—diluting their brand and confusing customers (to say nothing of investors) with an ever-changing array of unrelated products unrelated to the coffee business. From a marketing and strategy perspective, the firm has committed the deadly sins of creating “brand complexity, clutter and confusion.”

This is supposed to cause consumers to stay away in droves. For example, researchers at Stanford’s Graduate School of Business have found that firms that span a variety of product categories experience “penalties for generalism” in the marketplace. Using data from eBay and the US film industry, sociologists Greta Hsu, Mike Hannan and Özgecan Koçak showed that firms like Tchibo are viewed as “difficult to interpret” in terms of market categories, resulting in consumers “avoiding interaction with the uninterpretable producer and devaluing its offerings” (2009: 167).

A lively experiment by social psychologists Sheena Iyengar and Mark Lepper (2000) suggests how this works at the cognitive level.Their study presented participants with free samples of several fruit jams, then measured how many subsequently bought a jar. The researchers varied the experimental conditions so that one group of participants selected from a set of six different flavors of jam (the “limited-choice” condition), while the other group sampled from a set of 24 flavors (the “extensive-choice” condition). While both groups tried just one or two flavors, their purchasing behavior varied by an order of magnitude: only 3% ofthose in the “extensive-choice” group bought a jar of jam, compared to 30% in the “limited-choice” group.

And yet…Tchibo thrives despite its unpredictable and often chaotic-seeming array of product offerings. So far, the firm thrives only in Europe. And that may be a big clue to the mystery.

All the research cited in this post is based on studies conducted in North America.The assumption, usually unquestioned, is that these results are applicable everywhere. But the case of Tchibo, like the failure of Delhaize, presents some compelling empirical reasons to doubt the generalizability of marketing and strategy research, much of which comes out of universities in the US.

Is Germany just a special case of cultural misfit between research findings and consumer behavior? Or is the problem more widespread? Perhaps Tchibo will expand to the US and give us a chance to find out.

About Economic Sociology

Brooke Harrington explores the social underpinnings of money and markets. Read more…