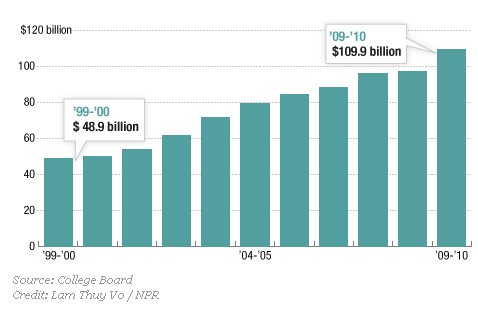

You’ve probably heard someone in media or politics bemoan the ballooning student debt in the U.S. In fact, debt has been rising. It’s more than doubled in the last ten years (that’s a more than 100% increase):

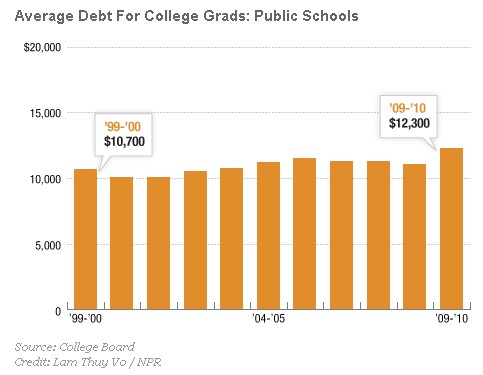

This debt, though, can’t be attributed primarily to the rising cost of education, as Planet Money explains. The average debt load for a student graduating from a public school, for example, has risen by 20%:

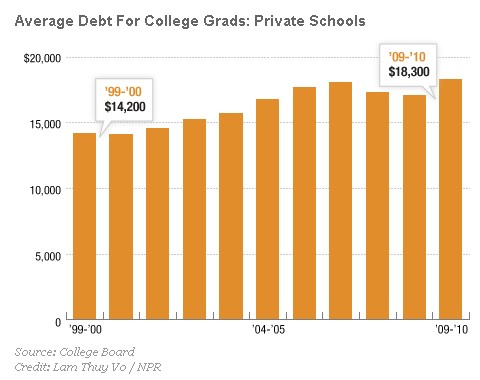

The average debt load for a student coming out of a private school has gone up a bit more, but still not enough to account for the leap in overall student debt.

The increase in debt, it turns out, is largely accounted for by an increase in the number of people going to college. In 1970, 8,500 8,500,000 people enrolled in college in the Fall; in 2009, that number exceeded 20,000 20,000,000 (source). A more than 100% increase.

So, the story isn’t quite as dire as we might think. This may be little consolation, though, for my students who walked across the stage yesterday. Congrats, Seniors! :)

Lisa Wade, PhD is an Associate Professor at Tulane University. She is the author of American Hookup, a book about college sexual culture; a textbook about gender; and a forthcoming introductory text: Terrible Magnificent Sociology. You can follow her on Twitter and Instagram.