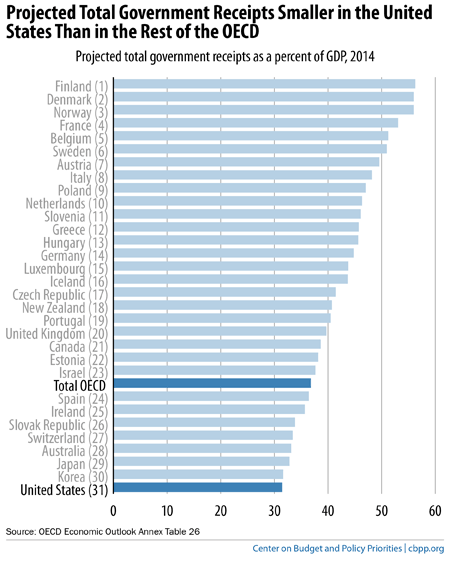

This chart comes from Chuck Marr at the Center on Budget and Policy Priorities. As Marr explains:

The United States is a relatively low-tax country, as the chart shows. When measured as a share of the economy, total government receipts (a broad measure of revenue) are lower in the United States than in any other member of the Organization for Economic Co-operation and Development (OECD), even after accounting for the modest revenue increases in the 2012 “fiscal cliff” deal and the taxes that fund health reform.

Martin Hart-Landsberg is a professor of economics at Lewis and Clark College. You can follow him at Reports from the Economic Front.