There was a great article in The Nation last week about social media and ad hoc credit scoring. Can Facebook assign you a score you don’t know about but that determines your life chances?

There was a great article in The Nation last week about social media and ad hoc credit scoring. Can Facebook assign you a score you don’t know about but that determines your life chances?

Traditional credit scores like your FICO or your Beacon score can determine your life chances. By life chances, we generally mean how much mobility you will have. Here, we mean a number created by third party companies often determines you can buy a house/car, how much house/car you can buy, how expensive buying a house/car will be for you. It can mean your parents not qualifying to co-sign a student loan for you to pay for college. These are modern iterations of life chances and credit scores are part of it.

It does not seem like Facebook is issuing a score, or a number, of your creditworthiness per se. Instead they are limiting which financial vehicles and services are offered to you in ads based on assessments of your creditworthiness.

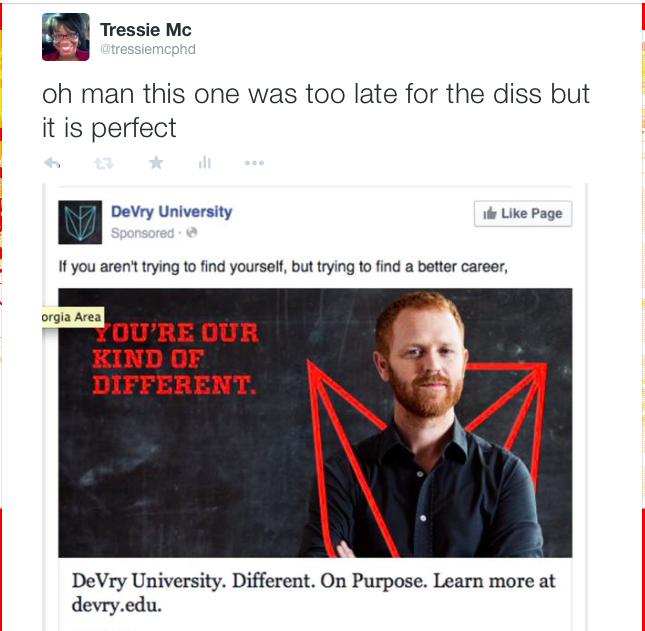

One of the authors of The Nation piece (disclosure: a friend), Astra Taylor, points out how her Facebook ads changed when she started using Facebook to communicate with student protestors from for-profit colleges. I saw the same shift when I did a study of non-traditional students on Facebook.

You get ads like this one from DeVry:

Although, I suspect my ads were always a little different based on my peer and family relations. Those relations are majority black. In the U.S. context that means it is likely that my social network has a lower wealth and/or status position as read through the cumulative historical impact of race on things like where we work, what jobs we have, what schools we go to, etc. But even with that, after doing my study, I got every for-profit college and “fix your student loan debt” financing scheme ad known to man.

Whether or not I know these ads are scams is entirely up to my individual cultural capital. Basically, do I know better? And if I do know better, how do I come to know it?

I happen to know better because I have an advanced education, peers with advanced educations and I read broadly. All of those are also a function of wealth and status. I won’t draw out the causal diagram I’ve got brewing in my mind but basically it would say something like, “you need wealth and status to get advantageous services offered you on the social media that overlays our social world and you need proximity wealth and status to know when those services are advantageous or not”.

It is in interesting twist on how credit scoring shapes life chances. And it runs right through social media and how a “personalized” platform can never be democratizing when the platform operates in a society defined by inequalities.

I would think of three articles/papers in conversation if I were to teach this (hint, I probably will). Healy and Fourcade on how credit scoring in a financialized social system shapes life chances is a start:

providers have learned to tailor their products in specific ways in an effort to maximize rents, transforming the sources and forms of inequality in the process.

And then Astra Taylor and Jathan Sadowski’s piece in The Nation as a nice accessible complement to that scholarly article:

Making things even more muddled, the boundary between traditional credit scoring and marketing has blurred. The big credit bureaus have long had sidelines selling marketing lists, but now various companies, including credit bureaus, create and sell “consumer evaluation,” “buying power,” and “marketing” scores, which are ingeniously devised to evade the FCRA (a 2011 presentation by FICO and Equifax’s IXI Services was titled “Enhancing Your Marketing Effectiveness and Decisions With Non-Regulated Data”). The algorithms behind these scores are designed to predict spending and whether prospective customers will be moneymakers or money-losers. Proponents claim that the scores simply facilitate advertising, and that they’re not used to approve individuals for credit offers or any other action that would trigger the FCRA. This leaves those of us who are scored with no rights or recourse.

And then there was Quinn Norton this week on The Message talking about her experiences as one of those marketers Taylor and Sadowski allude to. Norton’s piece summarizes nicely how difficult it is to opt-out of being tracked, measured and sold for profit when we use the Internet:

I could build a dossier on you. You would have a unique identifier, linked to demographically interesting facts about you that I could pull up individually or en masse. Even when you changed your ID or your name, I would still have you, based on traces and behaviors that remained the same — the same computer, the same face, the same writing style, something would give it away and I could relink you. Anonymous data is shockingly easy to de-anonymize. I would still be building a map of you. Correlating with other databases, credit card information (which has been on sale for decades, by the way), public records, voter information, a thousand little databases you never knew you were in, I could create a picture of your life so complete I would know you better than your family does, or perhaps even than you know yourself.

It is the iron cage in binary code. Not only is our social life rationalized in ways even Weber could not have imagined but it is also coded into systems in ways difficult to resist, legislate or exert political power.

Gaye Tuchman and I talk about this full rationalization in a recent paper on rationalized higher education. At our level of analysis, we can see how measurement regimes not only work at the individual level but reshape entire institutions. Of recent changes to higher education (most notably Wisconsin removing tenure from state statute causing alarm about the role of faculty in public higher education) we argue that:

In short, the for-profit college’s organizational innovation lies not in its growth but in its fully rationalized educational structure, the likes of which being touted in some form as efficiency solutions to traditional colleges who have only adopted these rationalized processes piecemeal.

And just like that we were back to the for-profit colleges that prompted Taylor and Sadowski’s article in The Nation.

Efficiencies. Ads. Credit scores. Life chances. States. Institutions. People. Inequality.

And that is how I read. All of these pieces are woven together and its a kind of (sad) fun when we can see how. Contemporary inequalities run through rationalized systems that are being perfected on social media (because its how we social), given form through institutions, and made invisible in the little bites of data we use for critical minutiae that the Internet has made it difficult to do without.

Tressie McMillan Cottom is an assistant professor of sociology at Virginia Commonwealth University. Her doctoral research is a comparative study of the expansion of for-profit colleges. You can follow her on twitter and at her blog, where this post originally appeared.

Comments 48

Japaniard — June 1, 2015

You actually read Facebook ads? And you read them often enough that you can notice when their contents change? Is this really a normal thing people do? I understand TV/radio ads that you would have to mute to avoid, but who actively reads the text of Facebook advertisements?

Shawna McComber — June 1, 2015

I use Ad Block and never ever see an ad on any webpage I go to ever.

Bill R — June 1, 2015

Buckle up. This is just starting. And don't expect the government to help you. They're in your knickers big time and enjoying the ride.

Fitness Gal — June 4, 2015

facebook needs to be regulated by government

our government is not doing its job

Andrew Maz — March 19, 2016

Check out the recent review on social tech trader and see if its a scam here this will blow your mind!

http://www.letstalkreviews.com/reviews/social-tech-trader-review/

osas weerty — September 11, 2016

Hello friends!!! My name is Walter brown. i want to testify of the good Loan Lender who showed light to me after been scammed by 3 different Internet international lender, they all promise to give me a loan after making me pay a lot of fees which yield nothing and amounted to no positive result. i lost my hard earn money and it was a total of 4,560,000USD. One day as i was browsing through the internet looking frustrated when i came across a testimony woman who was also scammed and eventually got linked to a legit loan company called michael frankfirm Plc and email:(michaelfrankfirm@hotmail.com) where she finally got her loan, so i decided to contact the same loan company and then told them my story on how i have been scammed by 3 different lenders who did nothing but to course me more pain. I explain to the company by mail and all they told me was not to cry no more because i will get my loan in their company and also i have made the right choice of contacting them. i filled the loan application form and proceeded with all that was requested of me and to my shock I was given a loan amount of $60,000.00 Dollars by this great Company (Michael frank-firm Plc} managed by Mrs Bevan Anderson a God fearing woman and here i am today happy because this company has given me a loan so i made a vow to my self that i will keep testifying on the internet on how i got my loan. Do you need a loan urgently? kindly and quickly contact This great company now for your loan via email:(michaelfrankfirm@hotmail.com)

Mr promise kings — October 11, 2016

Dear Applicant,

We give loan to private company and individuals. You can find some vital information about the loan we offer below. In getting a loan from our company, there are some information we need to pass across to you before we can proceed to the application process . INTEREST RATE: In the loan we offer, we do charge 3% Interest rate . AMOUNT GIVEN: We Give Out A Minimum Amount Of 1,000.00 to A Maximum of 100,000,000.00 INFORMATION NEEDED: As for the information needed, you will need to fill an application form which contains your personal information and also the loan information, this will help us give you a full documentation of the loan terms and agreement contract which you will be expected to sign and send back to the company for approval if satisfied. Email Us: (promisekingloancompany01@gmail.com)

ATM — February 9, 2017

Hello everyone am here to testify how i got my loan from Mr. Ben after i applied several times from various loan lenders who claimed to also testify right in this forum,i thought the testimonies where real and i applied but they never gave me loan. I was in need of an urgent loan to start a business and i applied from various loan lenders who promised to help but they never gave me the loan.Until a friend of mine introduce me to Mr. Ben Swart who promised to help me and indeed he did as he promised without any form of delay.I never thought there are still reliable loan lenders until i met Mr. Ben,who are indeed helped with the loan and changed my belief.I dont know if you are in any way in need of a genuine and urgent loan,free feel to contact Mr.Ben via his email{benlarryloanfunds@gmail.com

For Tuesday, Week 13 – Writing for New Media — April 21, 2017

[…] Read Chapters 10 and 12 in Understanding and “The Iron Cage.” […]

For Thursday, Week 13 – Writing for New Media — April 25, 2017

[…] Read Chapters 10 and 12 in Understanding and “The Iron Cage.” […]

Mulla Adman — July 12, 2017

Wilson Freeman

Hello

do you need a loan to start your own business do you want to buy a house or

a car if yes you need a loan you can whatsapp +2348142630659 email wilson

freeman via email wilsononlineloanoffer@gmail.con i got from him a legit

plan lender

Thompson Campbell — August 25, 2017

INSTANT LOAN FINANCIAL SERVICE have been accredited by the Better Business Bureau after meeting all their strict requirements.

If you're looking for an unsecured loan from non-bank sources, look no further and contact INSTANT LOAN FINANCIAL SERVICE today for just 2%

interest rate because it's great place to start your search. Borrowing money online is a fast and convenient option, but always keep safe by choosing a

reputable lender to work with. On some occasions, people find themselves in life scenarios where they need to borrow money for different reasons. It may be to make a large purchase, buy new home furniture's, finance a long awaited vacation or even to consolidate other debt, including high-rate interest card debt.they wouldn't even mind about the interest rate,but Getting a secured bank loan to do this can be difficult at times and it's not always accessible to regular, everyday clients.

PRODUCTS AND SERVICES RENDERED INCLUDE THE FOLLOWING

Applications by Phone, Auto & Mobile Home Leasing, Auto Title Loans, Cash Loans, Confidential Loans, Loans!, Same Day Approval, Signature & Auto Title, State Licensed, Title Loans,Debt Consolidation Loan,

Further more ILFS is governed under the C.E.O leadership of Mr Thompson Campbell

Contact us today on and put a stop to your financial misery in just 24 hours

contact us now on

email:

instantloanfinancialservice5@gmail.com

You can also text or call us on +1-(619) 784-7625 for further Inquiries

Best Regards

Thompson Campbell

C.E.O

Kayla Moore — September 9, 2017

INSTANT LOAN FINANCIAL

SERVICE HERE IN THE STATES PROMISED TO GRANT ME LOAN, AND WAS FINALLY APPROVED AND GIVEN A LOAN OF $45,500 to my greatest

surprise on the third day of my application,so I made a vow to Myself and God that I will keep sharing my testimony on the internet on how I got my loan.

you can contact them now and also put an end to your financial misery in less than 48 hours,call,text or email them now with the information below

Email Contact: instantloanfinancialservice5@gmail.com

Mobile Contact: +1-(619) 784-7625

Good Luck To Anyone Reading This Great Testimony That Happened To Me

Kayla C Moore

Resources – on automated systems and bias | Abeba Birhane — November 17, 2017

[…] The Iron Cage in binary code: How Facebook shapes your life chances – Sociological Images: December 30, 2015 […]

lisa — April 9, 2018

Good Day, My name is Lisa i am a citizen of the United State of America i want to testify of the good Loan Lender who showed light to me after been scammed by 4 different Internet international lender, they all promise to give me a loan after making me pay alot of fees which yield nothing and amounted to no positive result. i lost my hard earn money and it was a total of 8,000USD. One day as i was browsing through the internet looking forsterated when i came across a testimony man who was also scammed and eventually got linked to a legit loan company th citi bank loan (customercare@thecitibank.com) or visit www.thecitibank.com where he finally got his loan, so i decided to contact the same loan company and then told them my story on how i have been scammed by 4 different lenders who did nothing but to course me more pain. I explain to the company by mail and all they told me was to cry no more because i will get my loan in their company and also i have made the right choice of contacting them. i filled the loan application form and proceeded with all that was requested of me and I was given a loan amount of $600,000.00 Dollars by this great Company and here i am today happy with my family because the citi bank Loan Firm has given me a loan so i made a vow to my self that i will keep testifying on the internet on how i got my loan. Do you need a loan urgently? kindly and quickly contact Mr Jude Shanko Loan Firm now for your loan via email: (customercare@thecitibank.com) or visit www.thecitibank.com i believe other people are also giving testimony on this same honest lender

febian joan — May 6, 2018

Am joan from USA in Texas, I’m so happy, Frank Queen Loan Company has been so good to me and some of my friends we got our loans of US$ 700,000 from them, and i promise them if i get my loan i will help them post their ads online and testify their good work to people who are in need of a loan, if you need a legit loan today contact them via email: frankqueens64@gmail.com or whatsapp +2349057770649

williams bryce — May 7, 2018

Do you need a loan to pay off your bills or start a new business then

search no more,here we offer loan at 2% intest rate .

my Name is Mr william bryce we are certified loan Company who offer any kind

of financial assistance to people who are in need of it and here is

our mail feel free to send us a mail via:

williamsbryce505@gmail.com or you can also contact us on

whstspps number on +17853289627

jozey — June 18, 2018

Did you need a private financial loan to pay off your debt, or to start up

a new business?.. if yes contact us today via: unlimitedfunds1@gmail.com

for more details about our services.

private trust loan — June 19, 2018

Jó nap,

Sürgős hitelre van szüksége. Magánbiztosítási kölcsön azért van itt, hogy megadja azt a kölcsönt, Szeretné tisztázni az adósságát, az üzleti tevékenység bővítését vagy a személyes kölcsönöket ", akkor kapcsolatba léphet velünk a gyors és megbízható hitelével, 3% -os alacsony kamatlábon és megfizethető visszafizetéssel tervet a jó hitelviszonyokkal.Emil us: [privatetrustloan@consultant.com]

daniyal abbas — May 3, 2021

Karnataka board will release the 2nd PUC result 2021 one month after the conclusion of examinations. Students can check their Karnataka 2nd PUC result 2021 on the board's official results website - karresults.nic.in or from the board's official website - pue.kar.nic.inkarresults.nic.in PUC Result 2021 by providing their "Registration Number". Students can also make use of the direct link given on this page to download their PUC results 2021.

Gerard Wilson — May 10, 2021

The best way to make money now is to invest under a unique platform. I invested $1000 and earn $10,000 in just 24 hours of trading all thanks to Mr Gerard Wilson , He is the best I have ever met in my life. if you are interested, contact him via Facebook page https: https://www.facebook.com/Gerard.Wilson456 or WhatsAPP +1 (650) 533‑4554

Email: gerardwilson995@gmail.com

microblading — October 30, 2021

The coffee mug you sent is so me. Thank you for making my mornings brighter.

microblading

Peter Kyle — March 30, 2023

A social media strategy is a plan that will help you achieve your goals for social bell county roofing media. The plan will include specific strategies and tactics, as well as measurable goals. It doesn't need to be complicated, just specific and with measurable goals.

We offer money at 2% interest rate,apply now via: richardcosmos5@gmail.com — May 5, 2024

We offer money at 2% interest rate,apply now via: richardcosmos5(a)gmail.com

Wesley Gibson — September 27, 2024

Are you financially down? Do you need a loan to start up business or pay off bills? we offer all kinds of financial assistance to every individuals "Business loan and personal loan, for investment, debt consolidation and house purchase etc." we will be willing to offer you the loan contact us on our Email: (edgefinancialfirm@gmail.com) for more details.

Kind regards

Wesley Gibson

Finance Administrator

Email: edgefinancialfirm@gmail.com

Maria — October 23, 2024

WESTLAKE loans saved me from the dishonest and malicious people who excel in extorting money. they kindly granted me a loan of €50,000 over a period of 10 years, that is, a period of 120 months. so that I could invest in my various projects. I ask all those who have benefited from these services to come back and testify of their sincerity and honesty to the people, so that other people in need can also find a reliable refuge. I leave you their email address: Loanwestlake@gmail.com

telegram___https://t.me/loan59

Leoš Halbrstat — November 7, 2024

Využijte této skvělé nabídky od přímého investora bez nesmyslných poplatků od 20 000 Kč až do 50 000 000 Kč. Výši měsíčních splátek a dobu splatnosti lze přizpůsobit Vašim finančním možnostem. Zápis do registrů dlužníků ani vymáhání není překážkou. Jasná a srozumitelná smlouva. Osobní schůzku k podpisu úvěrové smlouvy lze domluvit i ve Vašem městě. Přihlaste se zdarma a nezávazně e-mailem: leoshalbrstat1@gmail.com

John Wilson — August 17, 2025

It feels good when you know you have a great credit profile. I was dying slowly inside until I opened up my situation to a colleague who then recommended JERRY LINK CREDIT GROUP, and narrated how they increased his score. I immediately, contacted via: jerrylinkgroup@gmail.com, I made some financial commitment upfront. Days after, all the negative on report cleared ,bankruptcy was removed completely, including foreclosure, and my score was raised to 789. I promised to let others know about their services. Do reach out to them via email. Thanks

PLVLÍNA PLACHKÁ — August 25, 2025

Půjčky s garancí na směnku i pro problémové klienty. Půjčka od soukromé osoby bez podvodu a bez poplatku za sjednání půjčky. Férové jednání a rychlé vyřízení. Veškeré informace o půjčce od soukromé osoby naleznete na emailové adrese:plachkaplvlina@gmail.com

NOVÁ HELENΝΑ — September 23, 2025

Dobrý den, hledáte finanční pomoc za rozumných podmínek a potřebujete peníze na svém bankovním účtu do 24 hodin? Jste zaměstnanec nebo osoba samostatně výdělečně činná, ale vaše banka vaši žádost zamítla? Máte nudný registr dluhů, kterých se jen tak nezbavíte? V každém případě vám mohu s vaším příjmem půjčit, kolik chcete. Požádejte o skvělé nebankovní financování za výhodných podmínek. Napište mi:hnova6241@gmail.com

ARNOLD — November 5, 2025

Losing $15,000 to fraud was heartbreaking. Thanks to JetWebHackers, I got my money back in 3 days. Their professionalism and dedication are unmatched. Contact them today! WhatsApp: +1(763)357-2550, email: jetwebhackers@gmail.com.

Kuchta Ondřej — December 12, 2025

Půjčka z České republiky

Dobrý den, potřebujete půjčku? Osobní půjčku? Podnikatelské půjčky? Pokud máte zájem, napište nám na (kuchtaondrej21@gmail.com) s níže uvedenými informacemi.

Vaše celé jméno:

Země:

Telefonní číslo:

Občanský průkaz:

Požadovaná částka:

Doba trvání:

Čekáme na vaši rychlou odpověď, děkujeme

Kuchta Ondřej — December 12, 2025

Vánoční nabídka půjčky

Nejlepší vánoční nabídka půjčky. Nabízíme vám velmi speciální rychlé a snadné hotovostní půjčky v rozmezí od 8 000 000 Kč do 10 000 000 EUR s úrokovou sazbou 3 %. S pomocí této konce roku můžete oslavit Vánoce a financovat svůj domov, podnikání, koupit si auto, koupit si motorku, založit si firmu. Napište nám: kuchtaondrej21@gmail.com

Kuchta Ondřej — December 12, 2025

Rychlá a spolehlivá půjčka od soukromé osoby

Dobrý den, byli jste podvedeni na mnoha místech a tentokrát hledáte poctivého člověka, který vám půjčí peníze právě zde. Toto je to správné místo, kde nabízíme půjčky pouze poctivým lidem. Naše půjčka se pohybuje od 2 000 Kč do 30 000 000 Kč nebo od 8 000 EUR do 80 000 000 EUR s velmi nízkou úrokovou sazbou po dobu 3 %. V případě zájmu nám prosím napište výši požadované půjčky, rok splácení půjčky, dobu trvání a kontaktujte nás emailem, abychom půjčku mohli velmi rychle získat. Napište nám: kuchtaondrej21@gmail.com

DR COLLI NS — December 19, 2025

Do you want to buy a kidney, body organ or want to sell a kidney or body organ? Are you looking for an opportunity to sell your kidney for money due to financial problems and you don't know what to do? Contact us today and we will offer you USD 800,000, for your kidney. My name is Dr. Dr Collins, I am a Neurologist and Medical Consultant at Our hospital specializes in Kidney Surgery. We also arrange Kidney Purchase and Transplant with Living Donors and Associates. We are locate worldwide USA and only serious minded people are needed. Please let us know if you are interested to sell or buy a kidney or . Please feel free to contact us via email and by email. Email: gw482053@gmail.com WhatApp via +1-920-251-9233 Best Regards,

narus — April 12, 2026

I was searching for a loan to sort out my bills & debts, then I saw comments about Blank ATM Credit Cards that can be hacked to withdraw money from any ATM machines around you I doubted this but decided to give it a try by contacting {rickatmcardoffer@gmail.com} they responded with their guidelines on how the card works. I was assured that the card can withdraw EUR 10,000 instant per day & was credited with EUR 50,000,000 so i requested for one & paid the delivery fee to obtain the card, after 24 hours later, i was shock to see the UPS agent in my resident with a parcel {card} i signed and went back inside and confirmed the card work after the agent left. This is no doubt because I have the card & have made use of the card. These hackers are Germany USA based hackers set out to help people with financial freedom!! Contact Mr Rick for help if you want to get rich with this and pay off your bills Via: rickatmcardoffer@gmail.com OR Whats-app via +1-920-251-9233 Best Regard

narus — April 12, 2026

I was searching for a loan to sort out my bills & debts, then I saw comments about Blank ATM Credit Cards that can be hacked to withdraw money from any ATM machines around you I doubted this but decided to give it a try by contacting {rickatmcardoffer@gmail.com} they responded with their guidelines on how the card works. I was assured that the card can withdraw EUR 10,000 instant per day & was credited with EUR 50,000,000 so i requested for one & paid the delivery fee to obtain the card, after 24 hours later, i was shock to see the UPS agent in my resident with a parcel {card} i signed and went back inside and confirmed the card work after the agent left. This is no doubt because I have the card & have made use of the card. These hackers are Germany USA based hackers set out to help people with financial freedom!! Contact Mr Rick for help if you want to get rich with this and pay off your bills Via: rickatmcardoffer@gmail.com OR Whats-app via +1-920-251-9233 Best Regard

Excel — May 25, 2026

Sürgősen hitelre van szüksége? Kínálunk személyi kölcsönt? Vállalkozási hitelek? Jelzálog? Mezőgazdasági hitelek? Oktatási hitelek? Adósságkonszolidációs hitel? Teherautó hitelek? Autó hitelek? Szállodai hitelek? Hitelek refinanszírozása? és még több adósság? Kezdő hitelek? .Ajánlat 2% kamattal! Elérhetőség: excelservices.managementonline@gmail.com

Mike Morgan — June 1, 2026

Good day,

Do you need an urgent loan to solve your financial needs, We provide loans from a minimum of $5,000.00 and a maximum of $500,000.00 for lasting comfort, 1-15 years at a very low interest rate of 3%. are reliable, efficient, fast and dynamic, with a 100% guaranteed loan also gives (euro, pound and dollar) Do you need a large capital to start your business or to expand? Have you lost hope and thought that there is no way out and financial burdens will remain? Do not hesitate to contact us for possible commercial cooperation: muthooth.finance@gmail.com Phone number: +917428831341 (Call/What's app)

* Home improvement

* Inventor loans

* Loan to consolidate debt

* Business loans

* commercial loan?

* personal loan?

* buy a car?

* refinance?

* mortgage?

Contact us today and we will be happy to do business with us Email: muthooth.finance@gmail.com Phone number: +917428831341 (Call/What's app)

loanwestlake@gmail.com — July 3, 2026

Whether you’re launching a new project, expanding your business, or facing an unexpected financial need, we provide reliable, customized financing solutions that make a real difference. Our goal is to support you with clear, straightforward terms and competitive interest rates—no hidden fees, no unnecessary delays.

* Loan amounts from €10,000 up to €2,500,000

* Flexible repayment plans designed to suit your unique situation

* Fast, professional approval process with dedicated support at every step

* Trusted by hundreds of clients who’ve successfully funded their projects :We understand how important timely financing is, which is why we make the process simple and transparent. Take the first step toward securing the funds you need today. Contact us now to get started: loanwestlake@gmail.com

WhatsApp: +15154259089