Cross-posted at Reports from the Economic Front.

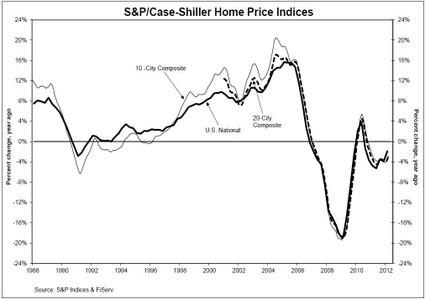

Economic recoveries often depend on the state of the housing market. While an April increase in housing prices has led many analysts to talk of a housing recovery, U.S. home values still remain depressed. According to a Zillow real estate research report, they are still some 25% below their 2007 peak.

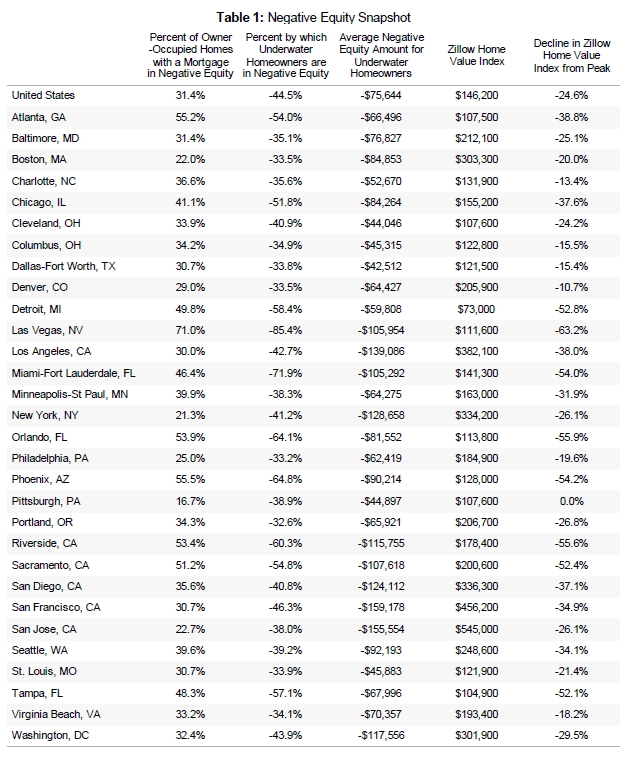

Perhaps the most telling indicator of the state of the housing market is that, as of the first quarter 2012, 31% of all owner-occupied homeowners with a mortgage were “underwater,” which means they had a mortgage greater than the market value of their home. As the table below shows, these homeowners owed, on average, $75,644 more than what their home was worth.

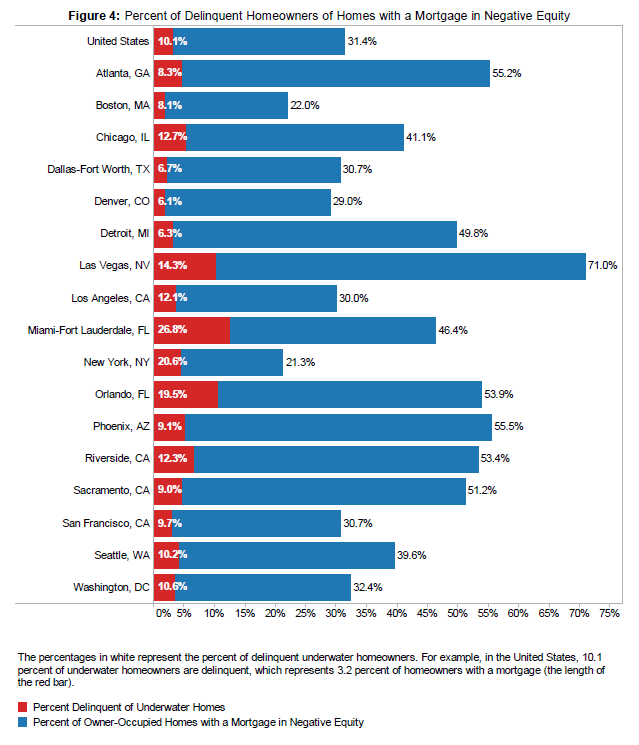

To this point, the high percentage of underwater homeowners represents, in the words of Zillow, only “a potential danger.” That is because “the majority of underwater homeowners continue to make regular payments on their mortgage, with only 10% percent of the 31% nationwide being delinquent.” The following figure highlights the percent of delinquent/underwater homeowners in the largest metropolitan areas.

At the same time, as Zillow notes:

With nearly a third of the nation’s mortgaged homeowners in negative equity and the average underwater homeowner having a home value that is 31 percent lower than their mortgage balance, negative equity will prove both to be difficult to fully eradicate near-term and to have pernicious effects longer term as some households continue to encounter short-term financial trouble even with a slowly improving broader economy. Should economic growth slow, more homeowners will not be able to make timely mortgage payments, thereby increasing delinquency rates and eventually foreclosures.

In other words, if the economy slows, or interest rates rise, two very likely possibilities, the housing market could deteriorate quickly, intensifying economic problems. In short, we are a long way from recovery.

Comments 9

Max Kingsbury — June 4, 2012

I love this blog but you consistently post graphs that are illegible because of their small size. Could you please start inserting higher resolution graphs?

Lily Queen — June 4, 2012

"Depressed" here means a 2-bedroom house that's 30+ years old and needs various work done and has no real yard in which to raise plants (for food etc.) still costs nearly half a million dollars. I have mixed feelings about this whole "recovery" thing. I have sympathy for people who bought fantastically overpriced houses using predatory loans, but do we need to inflate prices again? Teachers, librarians, and almost anyone who's not either a tenured professor or an engineer can't afford a house. The glut of people having to look for apartments keeps driving rent up, too.

SethTweddle — June 18, 2022

We buy houses in any condition, even if they need repair. We also buy properties with liens, back taxes, and foreclosures. Many sellers are struggling to sell their homes because they don’t want to pay for the commission required by real estate agents or because they don’t have enough time to fix up their property before it goes on the market. We understand these factors and offer a solution that works for everyone involved! We Buy Houses Memphis is a real estate company that buys houses in Memphis and the surrounding areas. We specialize in making the home buying process simple and easy. We can help you sell your house fast, regardless of its condition or situation. No matter what kind of situation you’re going through, we can help you get it off your hands.>https://www.webuyhomesinmemphis.com/

Oliver Green — September 26, 2022

I am sure that in any case, investments in real estate can still bring the most acceptable income. In my case, as the owner of an apartment in Toronto, I simply entrusted the solution of all issues to the specialists from RentCore, since they have been managing real estate in Canada for a long time, see More info here and personally I am absolutely satisfied with all the conditions and safety of my property.

Anna — February 9, 2023

While the housing market has recovered in some areas, it is still soft in other parts of the country. This has an impact on the economy, as people are less likely to invest in new businesses Tiny House or take on new jobs if they are worried about their house prices. If the housing market does not recover soon, the economy may continue to decline.

Frederic James — April 29, 2023

I seem to be struggling with some issues and tend to hire online businesses for sale advisors; doing so may provide hints on important preparations for making this step in the most efficient way possible This source is worth considering if you're interested in achieving maximum value from this deal.

Marcus Fernandez — January 16, 2024

If you are looking for a trusted online store with building materials, then now a large selection of everything that is required for construction, as well as for repairs, including MDF sheets, can be found here www.mgnbm.co.uk/18mm-standard-mdf-board-2440mm-x-1220mm-8-x-4/. Delivery is important for me, because I don’t have a car. This store offers free delivery across London and Essex on orders over £300